Summary

A surge in aircraft orders is responsible for the leap in durable goods for May, but even beneath the surface underlying orders activity perked up a bit. Still, durable shipments as well as other data out this morning on Q1 GDP, trade and jobless claims suggest a weaker first-half of the year for U.S. growth.

Sky high

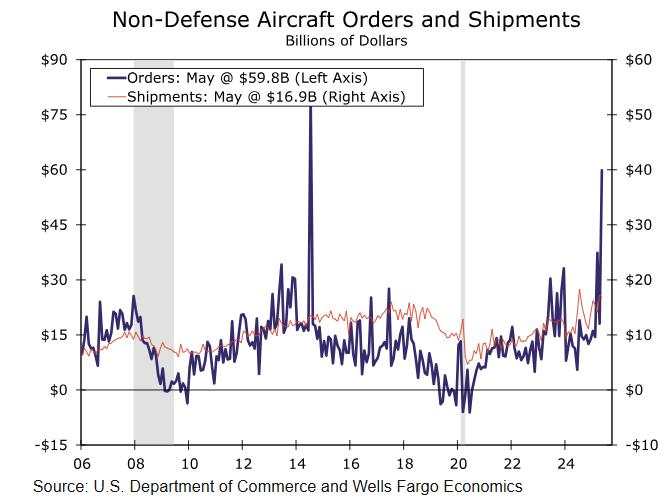

The 16.4% pop in durable goods orders in May is the biggest headline increase since 2014 when a bumper crop of aircraft orders boosted the headline number in a dramatic way. It is a similar story today with a 230.8% pop in civilian aircraft orders (chart). Rudyard Kipling famously suggested we meet with Triumph and Disaster and treat those two impostors just the same. The 26.4% increase in durable goods orders in July 2014 was followed by 21.2% drop the following month and back-to-back declines in every remaining month of that year. No one is saying that is what to expect in the remaining months of this year, but payback next month is very likely and our forecast looks for a soggy patch for capital investment in the second half.

The consensus expectation of a more modest (but still huge) increase of 8.5% was based on the widespread expectation that aircraft orders would rebound after a sharp decline in April. The better-than-expected out-turn here for aircraft is the big surprise, but there were pockets of strength in other areas as well. Defense spending posted a second-straight double-digit percentage increase and orders for computers & electronic products, electrical equipment as well as both primary and fabricated metals were all positive in May.

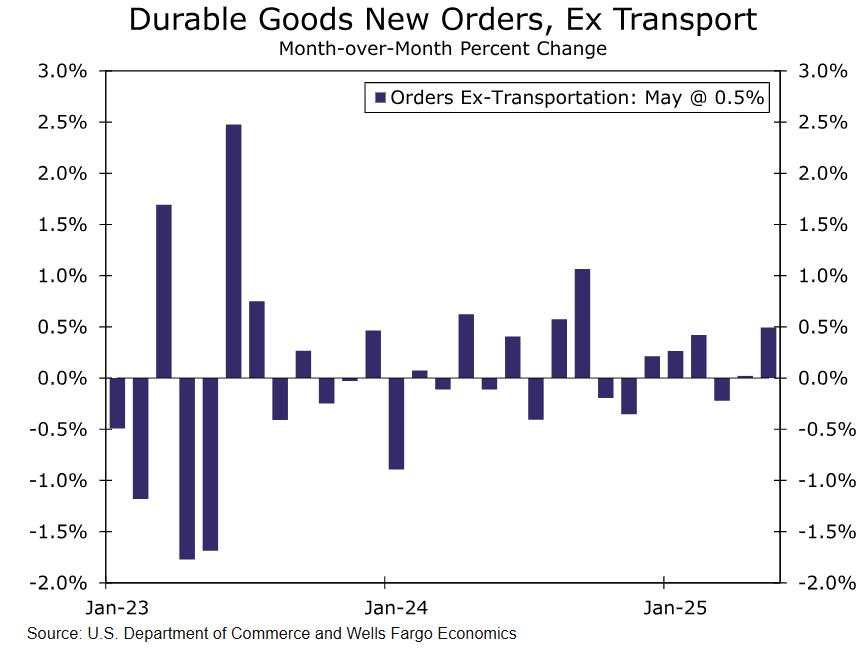

A theme in recent durable goods orders data has been a slowing in the underlying trend in orders. Admittedly, this has been hard to see amid big swings in aircraft and motor vehicle output. Excluding the transportation sector, durable goods orders had not moved more than half a percentage point in either direction since September 2024 (chart). Last month's increase in ex-transportation orders of 0.2% was revised away to leave no change for the month and today's print for this series came in at +0.5%.

Throughout the current cycle, decision makers have been preoccupied with intellectual property spending in a way that has made outlays in that space a priority, often at the cost of more modest equipment spending. The more-solid gain in computer & electronic orders (up 1.5% in May) is consistent with that trend. We ultimately expect continued uncertainty today hampers firms' broad willingness to invest.

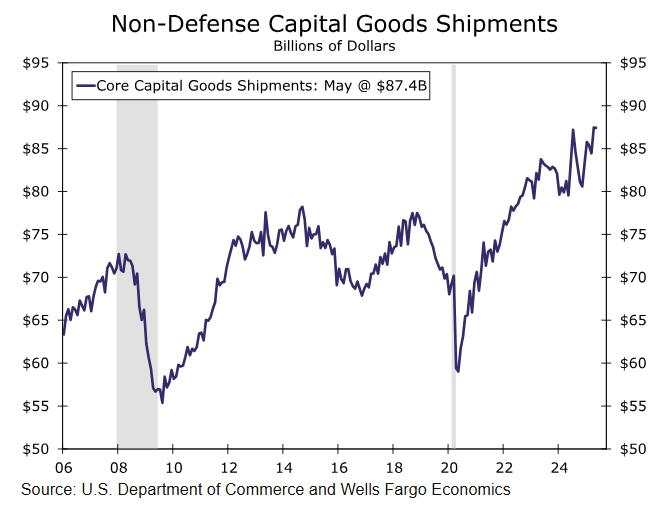

Durable goods shipments were also a bit stronger than anticipated. Excluding defense, capital goods shipments were flat in May when including aircraft (chart), and up half a percent when excluding air. This is still, however, consistent with a relatively weak outturn for real equipment investment in Q2. Beyond the durables data, that is sort of the theme of this morning's data. We got downward revisions to Q1 GDP growth mostly stemming from weaker services consumption implying less momentum behind the consumer. The number of people continuing to file claims for unemployment benefits is trending up. Advance data showing a collapse in exports and stalling in imports suggests the U.S. goods trade deficit widened in May and net exports may not boost growth as much as we previously anticipated. U.S. growth is shaping up to be a bit weaker in the first half of the year.

Download The Full Economic Indicator

作者:Wells Fargo Research Team,文章来源FXStreet,版权归原作者所有,如有侵权请联系本人删除。

风险提示:以上内容仅代表作者或嘉宾的观点,不代表 FOLLOWME 的任何观点及立场,且不代表 FOLLOWME 同意其说法或描述,也不构成任何投资建议。对于访问者根据 FOLLOWME 社区提供的信息所做出的一切行为,除非另有明确的书面承诺文件,否则本社区不承担任何形式的责任。

FOLLOWME 交易社区网址: www.followme.ceo

加载失败()