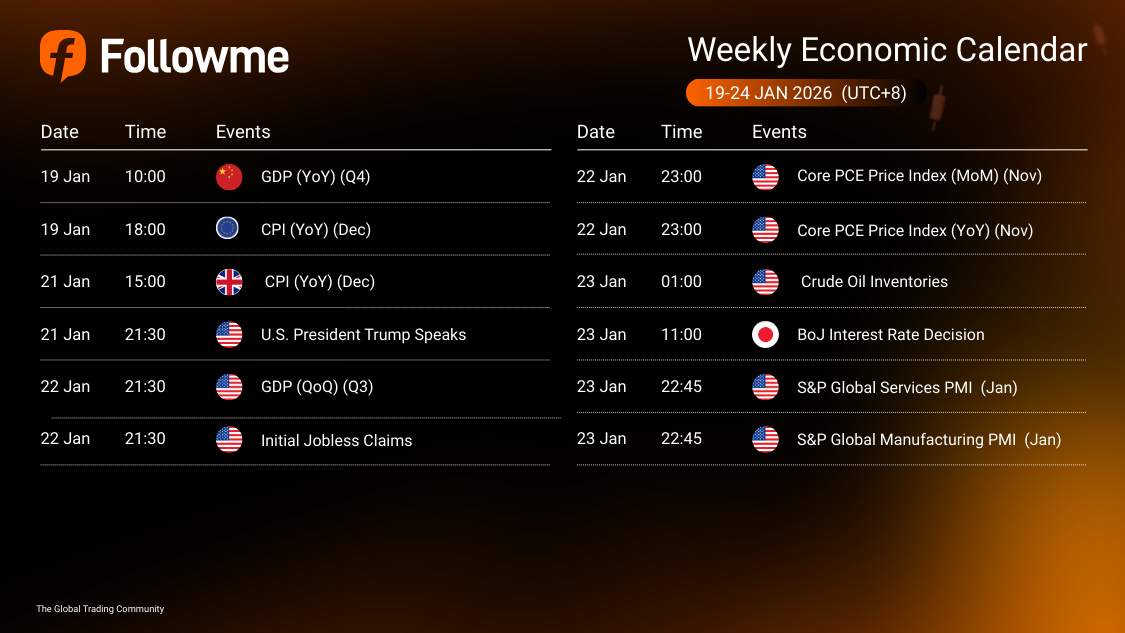

Weekly Economic Calendar: Week of January 19 - 24, 2026 (GMT+8)

This week’s macro calendar is driven by U.S. inflation (Core PCE) + late-week growth checks (S&P Global PMIs), with BoJ rate decision as the key Asia risk event. Early week, China GDP and Euro CPI can move broader risk tone, while UK CPI + UK GDP can swing GBP pricing. Expect the sharpest moves around U.S. Core PCE (Thu 23:00) and BoJ decision (Fri 11:00), with follow-through risk from oil inventories and PMIs later Friday.

| Time |

Cur. |

Events |

Fcst |

Prev |

| Monday, January 19, 2026 |

| 10:00 |

CNY |

GDP (YoY) (Q4) |

4.50% |

4.80% |

| 18:00 |

EUR |

CPI (YoY) (Dec) |

2.00% |

2.00% |

| Wednesday, January 21, 2026 |

| 15:00 |

GBP |

CPI (YoY) (Dec) |

3.30% |

3.20% |

| 21:30 |

USD |

U.S. President Trump Speaks |

|

|

| Thursday, January 22, 2026 |

| 21:30 |

USD |

GDP (QoQ) (Q3) |

4.30% |

3.80% |

| 21:30 |

USD |

Initial Jobless Claims |

203K |

198K |

| 23:00 |

USD |

Core PCE Price Index (MoM) (Nov) |

0.20% |

0.20% |

| 23:00 |

USD |

Core PCE Price Index (YoY) (Nov) |

2.70% |

2.80% |

| Friday, January 23, 2026 |

| 1:00 |

USD |

Crude Oil Inventories |

|

3.391M |

| 11:00 |

JPY |

BoJ Interest Rate Decision |

0.75% |

0.75% |

| 22:45 |

USD |

S&P Global Services PMI (Jan) |

52.8 |

52.5 |

| 22:45 |

USD |

S&P Global Manufacturing PMI (Jan) |

52.1 |

51.8 |

🇨🇳 GDP (YoY) (Q4) – Monday

🇪🇺 CPI (YoY) (Dec) – Monday

🇬🇧 CPI (YoY) (Dec) – Wednesday

🇺🇸 U.S. President Trump Speaks – Wednesday

🇺🇸 GDP (QoQ) (Q3) – Thursday

🇺🇸 Initial Jobless Claims – Thursday

🇺🇸 Core PCE Price Index (MoM) (Nov) – Thursday

🇺🇸 Core PCE Price Index (YoY) (Nov) – Thursday

🇺🇸 Crude Oil Inventories – Friday

🇯🇵 BoJ Interest Rate Decision – Friday

🇺🇸 S&P Global Services PMI (Jan) – Friday

🇺🇸 S&P Global Manufacturing PMI (Jan) – Friday

Macro Analysis

🇺🇸 U.S. Inflation Anchor (Core PCE MoM + YoY) – Thu: Core PCE is a top-tier input for Fed inflation framing. A hotter print (or less disinflation) tends to lift yields and support USD; a softer print can pull yields down and pressure USD, especially if markets lean into a “faster disinflation” narrative.

🇺🇸 U.S. Labour Pulse (Initial Claims) – Thu: Claims is the “growth stress check.” Lower-than-expected claims supports a tight-labour narrative (USD/yields supportive). Higher-than-expected claims can weaken risk tone and weigh on USD if yields fall.

🇺🇸 U.S. Activity Confirmation (S&P Global PMIs) – Fri: PMIs can validate (or fade) Thursday’s PCE-driven move. Stronger PMIs support a resilient-growth narrative; weaker PMIs can amplify growth concerns and increase two-way volatility into the close.

🇯🇵 BoJ Rate Decision – Fri: Even if the rate is unchanged, forward guidance can drive large moves in JPY crosses and spill over into global rates/risk. A surprise hawkish tilt can strengthen JPY and pressure USDJPY; a dovish tone can do the opposite.

🇺🇸 Crude Oil Inventories – Fri: Inventory surprises can swing oil quickly, feeding into inflation expectations and oil-sensitive FX. A big draw can lift crude and re-price inflation hedges; a big build can pressure crude and cool inflation fears.

🇬🇧 UK CPI + UK GDP – Wed/Thu: UK CPI shapes BOE expectations; UK GDP can shift the growth narrative. Big surprises can move GBP pairs and spill into broader USD positioning via risk and rate repricing.

🇨🇳🇪🇺 China GDP + Euro CPI – Mon: China GDP can set the week’s early risk tone (Asia + commodities sensitivity). Euro CPI can shift EUR rates expectations and influence USD via relative-yield repricing

Speculative Outlook for USD Traders

This is a CPI + Retail Sales week, expecting positioning to shift fast as inflation and demand data either confirm (or contradict) the rates narrative.

🟢 Bullish USD Scenario

Core PCE (MoM and/or YoY) prints firmer than expected (sticky inflation signal)

Claims come in below forecast (labour stays tight)

PMIs hold up / improve (growth stays resilient)

Oil inventories show a draw that lifts crude and inflation expectations

🔴 Bearish USD Scenario

Core PCE comes in softer (disinflation narrative strengthens)

Claims print above forecast (growth cooling signal)

PMIs soften (risk sentiment weakens, yields pressured)

Oil inventories show a build (crude pressured, inflation fears cool)

🟡 Wild Cards (High Whipsaw Risk)

MoM vs YoY Core PCE sending mixed signals

Speech-driven volatility (policy/geopolitical tone impacting risk)

BoJ guidance surprising markets and triggering fast repositioning in USDJPY

Watch the full calendar at Followme Economic Calendar Tool

Don’t forget to follow Followme and stay in sync with the latest updates.

暂无评论,立马抢沙发