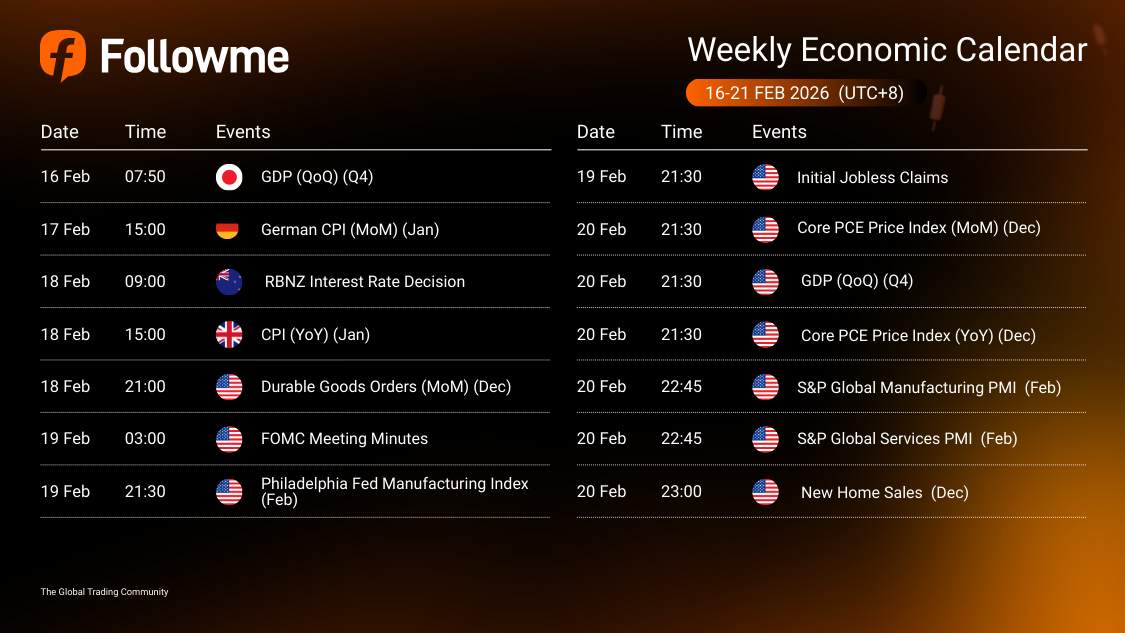

Weekly Economic Calendar: Week of February 16 - 21, 2026 (GMT+8)

This week’s macro calendar is driven by the FOMC Meeting Minutes (Thu 03:00) as the main USD volatility anchor (UTC+8). Mid-week, RBNZ Interest Rate Decision (Wed 09:00) is the key NZD risk event, while UK CPI (YoY) (Wed 15:00) and U.S. Durable Goods Orders (Wed 21:00) can add meaningful inflation and growth-driven swings. Later in the week, U.S. Initial Jobless Claims (Thu 21:30) and the U.S. Philadelphia Fed Manufacturing Index (Thu 21:30) shape near-term rates and activity expectations.

| Time | Cur. | Events | Fcst | Prev |

| JPY | GDP (QoQ) (Q4) | |||

| EUR | German CPI (MoM) (Jan) | |||

| RBNZ Interest Rate Decision | ||||

| CPI (YoY) (Jan) | ||||

| Durable Goods Orders (MoM) (Dec) | ||||

| Philadelphia Fed Manufacturing Index (Feb) | ||||

| Initial Jobless Claims | ||||

| Core PCE Price Index (MoM) (Dec) | ||||

| GDP (QoQ) (Q4) | ||||

| Core PCE Price Index (YoY) (Dec) | ||||

| S&P Global Manufacturing PMI (Feb) | ||||

| S&P Global Services PMI (Feb) | ||||

| New Home Sales (Dec) |

| Key highlights: |

🇯🇵 GDP (QoQ) (Q4) – Monday 07:50

🇩🇪 German CPI (MoM) (Jan) – Tuesday 15:00

🇳🇿 RBNZ Interest Rate Decision – Wednesday 09:00

🇬🇧 CPI (YoY) (Jan) – Wednesday 15:00

🇺🇸 Durable Goods Orders (MoM) (Dec) – Wednesday 21:00

🇺🇸 FOMC Meeting Minutes – Thursday 03:00

🇺🇸 Philadelphia Fed Manufacturing Index (Feb) – Thursday 21:30

🇺🇸 Initial Jobless Claims – Thursday 21:30

🇺🇸 Core PCE Price Index (MoM) (Dec) – Friday 21:30

🇺🇸 GDP (QoQ) (Q4) – Friday 21:30

🇺🇸 Core PCE Price Index (YoY) (Dec) – Friday 21:30

🇺🇸 S&P Global Manufacturing PMI (Feb) – Friday 22:45

🇺🇸 S&P Global Services PMI (Feb) – Friday 22:45

🇺🇸 New Home Sales (Dec) – Friday 23:00

Macro Analysis:

🇯🇵 Japan Growth Anchor (GDP QoQ, Q4) – Mon: Sets the early-week Asia tone. A stronger print supports JPY risk-on confidence; a weaker print can lean defensive and lift safe-haven flows.

🇩🇪 EUR Inflation Pulse (German CPI MoM, Jan) – Tue: Key EUR risk-tone driver for the week. A hotter print can firm EUR via rate expectations; a softer print does the opposite.

🇳🇿 RBNZ Policy Decision – Wed: The main NZD volatility point. Even without a surprise move, guidance and language can swing NZD pairs quickly (hawkish tilt supports NZD; dovish tilt pressures it).

🇬🇧 UK Inflation Signal (CPI YoY, Jan) – Wed: A rates-expectations mover for GBP. Upside inflation surprise tends to support GBP; downside can trigger repricing lower.

🇺🇸 U.S. Activity Pulse (Durable Goods Orders MoM, Dec) – Wed: A front-end growth check into the heavier U.S. block later in the week. Weakness can amplify growth worries; strength can support USD via relative yields.

🇺🇸 Fed Communication Anchor (FOMC Meeting Minutes) – Thu: The main USD volatility anchor this week. The catalyst is not “policy action” but how the minutes frame inflation progress, labour tightness, and the path for rates.

🇺🇸 U.S. Labour + Factory Stress Check (Initial Claims + Philly Fed) – Thu: A dual read on employment conditions and manufacturing momentum. Lower claims / stronger Philly tends to support USD and yields; deterioration can lean risk-off.

🇺🇸 U.S. Macro “Cluster” (Core PCE MoM/YoY + GDP QoQ, Q4) – Fri: The week’s biggest repricing window. Core PCE drives inflation expectations; GDP shapes the growth narrative—together they can reset rate-path pricing and USD direction.

🇺🇸 U.S. Activity Confirmation (S&P Global Manufacturing/Services PMI + New Home Sales) – Fri: Post-core data validation of momentum. Stronger prints support risk and USD through yields; weaker readings can fade any bullish repricing and revive slowdown concerns.

Speculative Outlook for USD Traders:

This is a Fed-minutes + late-week inflation/growth confirmation week, so positioning can reprice fast depending on rates expectations, yields, and Friday’s data cluster.

Check out full here: Followme Economic Calendar Tool

Follow Followme for the newest market updates

风险提示:本文所述仅代表作者个人观点,不代表 Followme 的官方立场。Followme 不对内容的准确性、完整性或可靠性作出任何保证,对于基于该内容所采取的任何行为,不承担任何责任,除非另有书面明确说明。

-THE END-